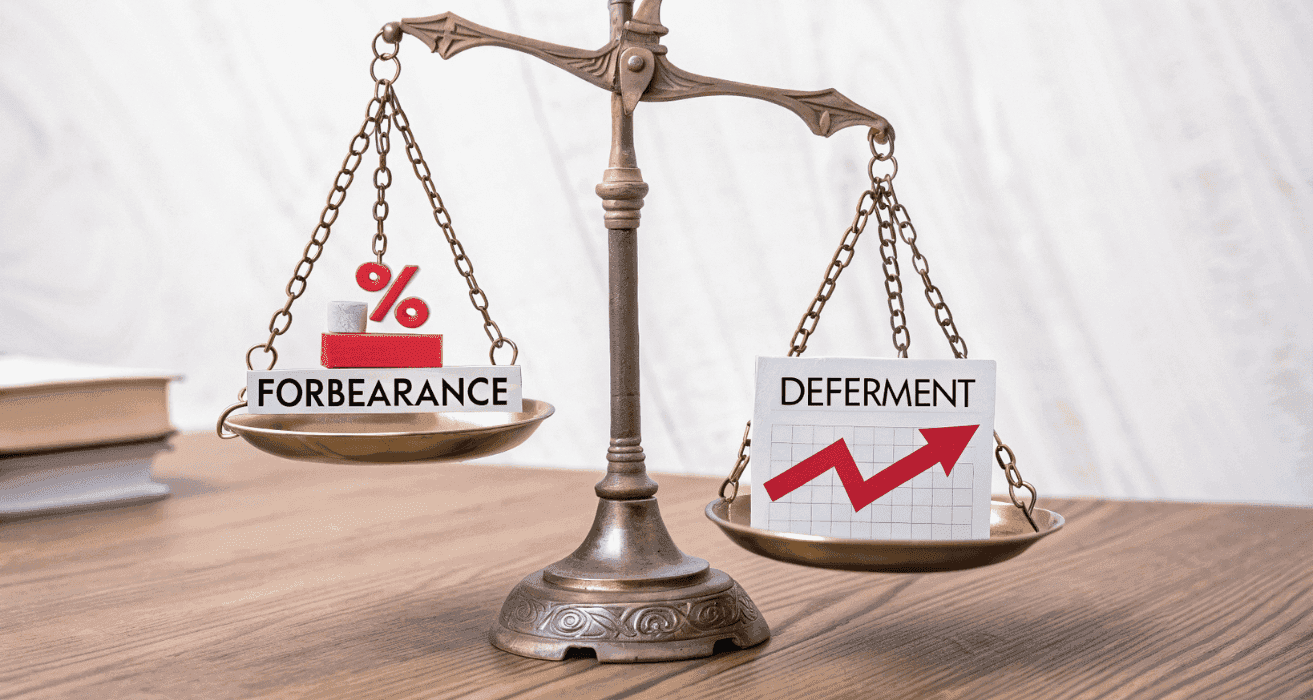

Forbearance vs. Deferment: Choosing Between Mortgage Relief Options

March 27, 2026

5 minutes

Let’s be honest, life throws curveballs. A job loss, medical emergency, or unexpected bill can put serious pressure on your monthly budget, especially when a mortgage is involved. If you're struggling to make payments, understanding your options is crucial. And that’s where two relief paths often come into play: forbearance and deferment.

They may sound similar, but they function very differently, and choosing the wrong one could cost you in the long run.

This guide will cut through the jargon, explain each option clearly, and help you make the smartest move for your financial future.

Forbearance pauses payments now, but you’ll need to repay them soon. Deferment moves skipped payments to the end of your loan. Choose based on when you can realistically repay, and get everything in writing.

Key Takeaways:

- Forbearance pauses your mortgage payments temporarily, but repayment comes due later.

- Deferment delays payments by moving them to the end of your loan term.

- Each option has pros and cons depending on your financial goals and loan terms.

- Relief options vary by lender; know your rights and ask the right questions.

- Always confirm any agreement in writing to protect yourself.

One application. 100+ lenders.

reAlpha Mortgage shops a network of lenders to find the right loan for your situation-no rate-shopping required.

What Is Forbearance?

Forbearance is a short-term pause or reduction in your monthly mortgage payments, usually granted during financial hardship.

How It Works:

- You don’t have to make full payments for a limited time.

- You must repay the skipped amounts later, often in a lump sum or via a repayment plan.

- Forbearance doesn't erase your debt, it only delays it.

Pro Tip: Always ask your lender how repayment will work before you agree. Some require a full lump sum immediately after the forbearance period ends.

Example: If your monthly mortgage is $1,500 and you enter a 3-month forbearance, that’s $4,500 in deferred payments. Unless you have a clear repayment plan, this could be a financial shock.

What Is Deferment?

Deferment allows you to push missed payments to the end of your loan term, instead of paying them right after the relief period.

How It Works:

- Payments are typically added as a non-interest-bearing balance or balloon payment at the end of your loan.

- Your monthly payment resumes as normal once the deferment period ends.

Real Talk: Deferment is often less financially stressful than forbearance, if your lender offers it.

Heads Up: Not all lenders offer true deferment. Sometimes they’ll call it a deferment but require a balloon payment sooner than expected. Read the fine print.

Side-by-Side Comparison

| Feature | Forbearance | Deferment |

|---|---|---|

| Payments Paused | Yes | Yes |

| Repayment Timing | Short-term (lump sum or plan) | Long-term (at the end of the loan) |

| Interest Accrual | Yes, unless waived | Typically yes |

| Credit Impact | Neutral if agreed upon and reported | Neutral if agreed upon and reported |

| Available To Whom | Varies by lender and hardship type | Varies, often more selective |

Get Pre-Qualified and Save Up to 1.5% at Closing with reAlpha

Save up to 1.5% at closing when you combine real estate and mortgage services with reAlpha.

Which One Should You Choose?

This depends on:

- Your timeline for financial recovery

- Lender flexibility

- Loan type (e.g., conventional, FHA, USDA; rules differ)

- Whether you can handle a lump sum later.

Pro Tip: Always confirm your relief option in writing. Verbal promises won’t hold up if a loan servicer changes hands.

What Lenders Say?

According to Freddie Mac and Fannie Mae guidance:

- Forbearance is usually the first step for hardship relief.

- Deferment is sometimes offered afterward, depending on your circumstances.

Check with your lender’s website for their specific relief programs. If you're unsure, call their mortgage relief department and ask:

- What are the repayment terms?

- Will interest accrue?

- Will this affect my credit?

- Can I refinance after this?

Conclusion: Buy Smart, Save Big with reAlpha

Choosing the right mortgage relief is just the first step - buying your next home wisely is where the real savings come in. With reAlpha, you can unlock a substantial portion of your buyer agent’s commission back, putting thousands of dollars toward closing costs, inspections, or move-in upgrades.

Here’s how it works:

- Receive a Cashback when you work with a reAlpha agent

- Increase your savings by adding reAlpha Mortgage

- Maximize your Cashback by bundling title services

Ready to turn savings into smart ownership? Explore your Cashback with reAlpha Mortgage.

FAQs

What’s the main difference between forbearance and deferment?

Forbearance is a temporary pause in payments, while deferment pushes payments to the end of the loan.

Does forbearance hurt your credit?

It shouldn't if it's properly reported and part of a formal agreement.

Can I sell my home while in forbearance or deferment?

Yes, but any missed payments will be settled during closing.

Do I have to pay interest during deferment?

Usually yes, unless your lender specifies otherwise.

Can I refinance after forbearance?

Often yes, but you may need to resume payments for a few months first.

Disclosure:

This blog is for informational purposes only and does not constitute financial advice. Mortgage relief options vary by lender and loan type - always consult your mortgage servicer directly. Licensing: reAlpha Mortgage is a licensed mortgage lender | NMLS #1743790. reAlpha operates as a technology platform and does not provide mortgage lending services. All mortgage-related services are offered through reAlpha Mortgage and are subject to standard underwriting criteria and disclosures.

Get the latest market trends, homebuying tips, and insider updates—straight to your inbox. No fluff, just the good stuff.

Article by

Rocky Billore is a mortgage industry leader and Chief Sales Officer with over two decades of experience across residential and commercial lending. Since entering the industry in 2004, he has been directly involved in funding more than $1.4 billion in loans. A recognized expert in VA and government lending, Rocky combines deep program knowledge with a data driven, relationship-first leadership style. His work focuses on building scalable sales organizations, developing high performing teams, and aligning technology with real world lending outcomes to improve the homeownership experience.