March 26, 2026

9 minutes

If you’re eligible for a VA loan, you may be sitting on one of the more valuable homebuying benefits available in the U.S.

A VA home loan is a mortgage backed by the U.S. Department of Veterans Affairs that helps eligible veterans, active-duty service members, and some surviving spouses buy a home with more favorable terms than many traditional loans.

Unlike many conventional mortgages, VA loans are designed to reduce upfront costs and increase buying power for those who served.

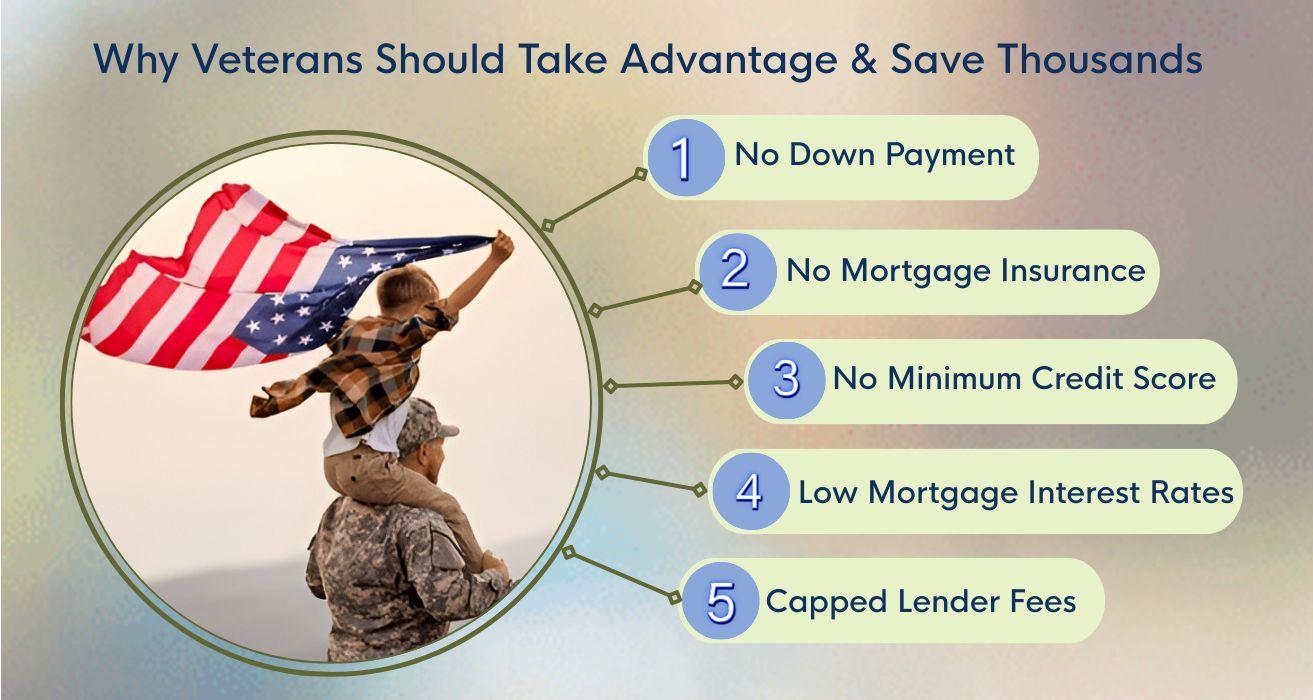

What Are the Benefits of a VA Loan?

Key VA loan benefits include:

- No down payment required for eligible borrowers

- No private mortgage insurance (PMI)

- Competitive VA mortgage rates compared with many loan types

- Flexible credit guidelines for qualifying borrowers

- Limits on certain closing costs

Reusable lifetime benefit that can be used more than once

These advantages can significantly reduce both the upfront cash needed to buy a home and the monthly payment burden, which is why VA loans are one of the among the more valuable benefits availab to military families.

Want the a quick way to check whether you qualify before you run numbers? You can start with this overview of VA loan eligibility so you don’t miss a simple requirement that could delay your timeline.

Why Many Veterans Choose VA Loans

Compared with many other mortgage options, VA loans often make it easier for qualified buyers to purchase a home sooner.

For example:

Loan Type | Typical Down Payment | PMI Required |

|---|---|---|

| VA Loan | 0% | No |

| Conventional Loan | 3–20% | Yes (if <20%) |

| FHA Loan | 3.5% | Yes |

Because VA loans don’t require PMI and may allow zero down, eligible buyers may keep more cash available for savings, emergencies, or moving expenses.

Before you shop homes, get a clearer “yes/no + price range” by learning the difference between prequalification vs preapproval (most buyers confuse these and lose weeks).

One application. 100+ lenders.

reAlpha Mortgage shops a network of lenders to find the right loan for your situation-no rate-shopping required.

The 6 Biggest VA Home Loan Benefits (With illustrative examples)

VA home loan benefits aren’t just marketing points-they translate into real dollars saved at closing and over the life of the loan. Below are six of the most powerful advantages eligible buyers can use to increase affordability and buying power.

If you want a real benchmark for what “competitive” looks like right now, compare options by shopping your rate across a network of lenders (it helps you spot whether a quote from a lender in the network is actually strong)

No Down Payment (0% Down) - What You Save at Closing

One of the most well-known VA home loan benefits is the ability for eligible buyers to purchase a home with no down payment requirement.

For many buyers, the down payment is the biggest barrier to homeownership.

Example savings on a $350,000 home

Loan Type | Typical Down Payment | Cash Needed |

|---|---|---|

| VA Loan | 0% | $0 |

| Conventional (5%) | $17,500 | $17,500 |

| Conventional (20%) | $70,000 | $70,000 |

That means eligible buyers could keep tens of thousands of dollars in savings rather than using it for a down payment.

Should you still put money down?

Sometimes. A small down payment may reduce the VA funding fee or monthly payment. Many buyers choose 0% down to preserve liquidity.

A veteran buying a $350K home could keep $17,500-$70,000 in cash compared with typical conventional loans.

No PMI Monthly Savings vs Conventional and FHA

Most mortgages require private mortgage insurance (PMI) when the down payment is less than 20%. VA loans do not require PMI, which can significantly reduce monthly costs.

Typical PMI ranges from 0.5%-1% of the loan amount annually.

Example monthly cost on a $350,000 loan

Loan Type | Monthly PMI |

|---|---|

| VA Loan | $0 |

| Conventional | $150–$300 |

| FHA Mortgage Insurance | $200–$280 |

Assumptions: ranges vary based on credit score, loan size, and lender guidelines.

Money impact: Avoiding PMI could save $1,800-$3,600 per year.

Competitive VA Rates - When 0.5% Lower can make a meaningful difference

VA-backed mortgages often offer competitive interest rates compared with many conventional loans, which can make a a noticeable difference over time.

Example lifetime interest difference on a $350,000 loan

Interest Rate | Monthly Payment | Total Interest (30 years) |

|---|---|---|

| 6.5% | $2,212 | $446,000 |

| 6.0% | $2,098 | $405,000 |

Even a 0.5% lower rate could reduce lifetime interest by tens of thousands of dollars.

Money impact: A 0.5% rate difference could mean $40,000+ in potential lifetime interest savings.

More Flexible Approval (Credit, DTI, Residual Income)

VA loans are designed to help eligible borrowers qualify for home financing while still maintaining responsible lending standards.

Lenders typically review several factors during approval:

- Credit history

- Debt-to-income ratio (DTI)

- Stable income

- Residual income requirements

- Certificate of Eligibility (COE)

Because VA underwriting considers residual income guidelines, some borrowers may qualify even when other loan programs are more restrictive.

Approval always depends on lender underwriting and borrower qualifications.

Money impact: Greater flexibility may allow eligible buyers to enter the housing market sooner instead of waiting years to save a larger down payment.

Closing Cost Protections + Seller Concessions

Another important VA loan benefit is the limit on certain fees and the possibility for seller concessions.

VA rules restrict some charges that borrowers might otherwise pay in other loan programs.

In some transactions, sellers may agree to cover certain costs such as:

- Closing costs

- Discount points

- Prepaid property taxes or insurance

- Certain debt payoffs (within VA guidelines)

In competitive markets, this can reduce the cash needed to close.

Money impact: Seller concessions may reduce upfront costs by thousands of dollars at closing, depending on the transaction.

No Prepayment Penalty

VA loans generally do not include a prepayment penalty, which means borrowers can:

- Pay extra toward the principal

- Refinance later

- Pay off the loan early

Without penalties for early payoff, homeowners may reduce total interest costs over time if they make additional payments or refinance when appropriate.

Money impact: Making extra payments or refinancing could potentially reduce total interest paid over the life of the loan, depending on borrower circumstances.

VA Loan Benefits for Disabled Veterans

For many service members, VA loan benefits for disabled veterans can make homeownership significantly more affordable.

One of the biggest advantages is that eligible veterans with a service-connected disability may be exempt from the VA funding fee, which is normally charged on VA loans. In many cases, veterans with a 10% or higher disability rating may qualify for this exemption, depending on their eligibility status.

The funding fee is typically a percentage of the loan amount and can range from about 1.25% to 3.3%, depending on the loan type and whether it’s the borrower’s first VA loan.

If you’re trying to estimate what your disability rating could mean for housing math, use this guide on VA disability rates as a quick reference point.

What That Could Mean in Real Dollars

Home Price | Typical VA Funding Fee (2.15%) | With Disability Exemption |

|---|---|---|

| $300,000 | $6,450 | $0 |

| $400,000 | $8,600 | $0 |

| $500,000 | $10,750 | $0 |

For eligible borrowers, this exemption can eliminate thousands of dollars in upfront loan costs.

Money impact: A disabled veteran buying a $400,000 home could avoid around $8,600 in funding fees.

Additional VA Home Loan Benefits for Disabled Veterans

In addition to the funding fee exemption, disabled veterans may also qualify for other financial advantages.

These benefits can vary depending on state and local programs.

Common examples include:

- Property tax exemptions in some states for veterans with qualifying disability ratings

- Specially Adapted Housing (SAH) grants that may help fund accessibility improvements

- Special Housing Adaptation (SHA) grants for modifying existing homes

- Potential local housing assistance programs offered through state or municipal agencies

Because these benefits vary by location, eligibility rules and available programs may differ by state and local jurisdiction.

Why This Benefit Matters

When combined with other VA loan benefits - such as no down payment and no PMI - the funding fee exemption can significantly reduce the total cost of buying a home.

For many eligible disabled veterans, this creates one of the one of the more cost-efficient mortgage options depending on your situation.

Money impact: Eliminating the funding fee alone could reduce upfront costs by $6,000-$10,000+ depending on the home price.

VA Loan Pros and Cons (Honest Breakdown)

VA loans offer powerful advantages, but like any mortgage program, they also come with a few tradeoffs. Understanding both sides helps veterans decide when a VA loan is the smartest option-and when to plan around potential drawbacks.

Pros of a VA Loan

Most eligible buyers choose VA financing because of these core benefits:

- No down payment requirement for eligible borrowers

- No private mortgage insurance (PMI)

- Competitive mortgage interest rates compared with many loan types

- Flexible credit and income guidelines

- Limits on certain closing costs

For many borrowers, these benefits reduce the cash needed to buy a home and the monthly payment burden.

Potential Downsides to Understand

While VA loans are powerful tools, there are a few considerations to keep in mind:

VA funding fee

Most borrowers pay a one-time funding fee that helps support the VA loan program. However, this fee can typically be rolled into the loan amount instead of paid upfront, and some disabled veterans may qualify for a full exemption.

If you want to see the funding fee broken down with who pays what (and how to reduce it), this dedicated guide makes it easier to plan

VA appraisal and Minimum Property Requirements (MPRs)

VA loans require an appraisal that ensures the home meets certain safety and livability standards. While this protects buyers, it can occasionally lead to repairs being required before closing.

Primary residence requirement

VA loans are intended for primary residences, meaning the borrower must plan to occupy the home.

Lower starting equity with 0% down

Buying with no down payment means you begin with little or no equity, which could matter if home values decline.

How to Reduce the Downsides (Funding Fee, Appraisal, Equity)

The good news is that many of these potential downsides can be managed with smart planning.

The VA funding fee depends on factors such as loan type, down payment, and whether it’s your first VA loan.

Ways borrowers sometimes reduce this cost include:

- Making a down payment of 5%-10%, which may lower the funding fee percentage

- Checking eligibility for disability-related exemptions

- Understanding how reuse of VA benefits may affect the fee structure

Because the fee can often be financed into the loan, many buyers avoid paying it out of pocket at closing.

How to Avoid VA Appraisal Surprises

Since VA appraisals verify that homes meet Minimum Property Requirements, preparing ahead can prevent delays.

Helpful steps include:

- Confirm the property has working utilities, safe access, and sound structural conditions

- Watch for common issues like roof damage, peeling paint in older homes, or safety hazards

- Consider a pre-offer inspection checklist to identify potential issues early

These precautions can help reduce the risk of appraisal-related delays.

When It Might Make Sense to Put 5-10% Down

Although VA loans allow 0% down, some buyers choose to put money down strategically.

Situations where this may help include:

- Reducing the VA funding fee percentage

- Lowering the monthly mortgage payment

- Building initial equity in the home

For example, a buyer putting 5-10% down on a $400,000 home may start with $20,000-$40,000 in equity, which can provide additional financial flexibility.

VA Loan vs Conventional vs FHA (which-loan-for-you matrix)

Choosing the right mortgage isn’t just about rates-it’s about which loan may fit your financial situation and goals.

While VA loan benefits can be extremely powerful, conventional and FHA loans may still make sense in certain cases. The key is understanding which loan type works best for different buyer profiles.

Quick Comparison: VA vs Conventional vs FHA

Feature | VA Loan | Conventional Loan | FHA Loan |

|---|---|---|---|

| Down payment | 0% possible | 3-20% | 3.5% |

| PMI / Mortgage Insurance | None | Required <20% | Required |

| Credit flexibility | Moderate-Flexible | Moderate-Strict | Flexible |

| Occupancy | Primary residence | Primary / second / investment | Primary residence |

Because VA loans remove both down payment and PMI requirements, they often provide the lowest upfront cost for eligible borrowers.

Which Loan Type Is Best for You?

Buyer Type | the disabled Veterans Type | Why |

|---|---|---|

| First-time buyer with limited savings | VA Loan | No down payment and no PMI reduce upfront costs |

| Borrower with higher debt-to-income ratio | VA Loan | Residual income guidelines may provide flexibility |

| Buyer with strong credit + 20% down | Conventional Loan | Avoid PMI and may secure competitive rates |

| Short-term homeowner (moving soon) | Conventional Loan | Avoid VA funding fee if equity is already available |

| Multi-unit house-hack buyer | VA Loan | Up to 4 units allowed if borrower occupies one |

| Investor buying rental property | Conventional Loan | VA loans require primary occupancy |

for eligible Veterans and service members, the VA loan often offers the a significant affordability advantage, especially when buyers want to preserve savings or minimize monthly payments.

How Many Times Can You Use a VA Loan Benefit?

One of the most misunderstood VA loan benefits is that it’s not a one-time program.

Eligible borrowers can often use the VA loan benefit multiple times throughout their lifetime, as long as entitlement is available.

Think of VA Entitlement Like a “Credit Line”

The VA doesn’t lend the money directly. Instead, it guarantees a portion of the loan to the lender, which helps reduce risk.

This guarantee is called VA entitlement.

In simple terms, entitlement works somewhat like a credit line backed by the VA that supports your mortgage.

Full vs Partial Entitlement

There are two main entitlement situations:

Full entitlement

You may have full entitlement if:

- You’ve never used a VA loan before, or

- A previous VA loan was paid off and the property was sold

With full entitlement, many borrowers can purchase a home without a loan limit in most areas, provided they qualify with the lender.

Partial entitlement

Partial entitlement happens when a previous VA loan has not been fully restored.

This may occur if:

- You still own a home purchased with a VA loan

- Your entitlement is tied up in an existing VA mortgage

In this case, you may still be able to use remaining entitlement, but borrowing limits could apply depending on your situation.

Restoring Your VA Loan Benefit

Many borrowers restore their full entitlement after:

- Selling the home purchased with a VA loan

- Paying off the VA loan balance

Once restored, the benefit can often be used again for another home purchase.

When Loan Assumptions Can Tie Up Entitlement

VA loans are assumable, meaning another buyer can sometimes take over the existing mortgage.

However, if the buyer assumes the loan is not eligible for VA benefits, your entitlement may remain tied to that loan until it’s fully repaid.

Because of this, borrowers should understand how loan assumptions could affect future use of their VA loan benefit.

This ability to reuse the benefit is one reason VA loans remain one of the most flexible mortgage programs available to eligible military borrowers.

Get Pre-Qualified and Save Up to 1.5% at Closing with reAlpha

Save up to 1.5% at closing when you combine real estate and mortgage services with reAlpha.

VA Refinance Benefits (IRRRL vs Cash-Out)

VA loan benefits don’t end after you buy a home. Eligible borrowers may also use VA refinance programs to potentially lower their interest rate, reduce monthly payments, or access home equity.

The two most common options are the VA Interest Rate Reduction Refinance Loan (IRRRL) and the VA Cash-Out Refinance.

VA IRRRL (Interest Rate Reduction Refinance Loan)

The VA IRRRL, often called a VA Streamline Refinance, allows borrowers with an existing VA loan to refinance into a new VA loan-usually with less paperwork and fewer requirements.

This option may make sense when:

- Interest rates drop and you want to reduce your monthly payment

- You want to switch from an adjustable-rate mortgage (ARM) to a fixed rate

- You want a simpler refinance process

Key characteristics of IRRRL:

- Typically less documentation than standard refinances

- Often no new appraisal required

- Lower VA funding fee compared with purchase loans

- The loan must generally provide a tangible benefit, such as a lower rate

Example monthly impact

Loan Balance | Old Rate | New Rate | Monthly Payment Change |

|---|---|---|---|

| $350,000 | 6.75% | 6.00% | ~$170 lower |

Actual savings vary depending on loan terms and lender requirements.

VA Cash-Out Refinance

The VA Cash-Out Refinance allows eligible homeowners to replace their current mortgage with a new VA loan and withdraw equity from the home as cash.

Common uses include:

- Paying off higher-interest debt

- Funding home renovations

- Covering major expenses

Refinancing a non-VA loan into a VA loan

Example scenario:

Home Value | Current Loan Balance | Possible Cash-Out |

|---|---|---|

| $450,000 | $300,000 | Up to ~$150,000 (depending on lender guidelines) |

However, cash-out refinancing increases the total loan balance, which means borrowers should carefully evaluate long-term costs.

Key risk to consider: Taking equity out increases your mortgage debt and could extend the repayment timeline.

The VA Homebuying Process (COE → Offer → Closing) in 7 Steps

Understanding how the VA homebuying process works can make the experience smoother and help veterans compete more confidently in the housing market.

Here is a simplified 7-step roadmap from eligibility to closing.

1. Obtain Your Certificate of Eligibility (COE)

The Certificate of Eligibility (COE) confirms that you qualify for VA loan benefits.

It verifies:

- military service eligibility

- available VA entitlement

- qualification for VA loan programs

lenders within the network can help obtain the COE electronically during the application process.

2. Get Pre-Approved With a VA-Approved Lender

A pre-approval helps determine:

- estimated loan amount

- potential monthly payment

- purchasing power

This step also strengthens your offer when you begin house hunting.

3. Begin Your Home Search

Once pre-approved, buyers typically work with a real estate agent to find homes that meet both budget and VA property requirements.

VA loans can be used for:

- single-family homes

- approved condos

- multi-unit properties (up to 4 units) if the borrower occupies one unit

4. Make a Competitive Offer

When you find the right home, your agent helps structure an offer.

Some strategies that can strengthen a VA-backed offer include:

- strong pre-approval documentation

- flexible closing timelines

- clear communication with the seller

5. VA Appraisal and Minimum Property Requirements (MPRs)

Once the offer is accepted, the lender orders a VA appraisal.

The appraisal verifies two things:

- the home’s market value

- compliance with Minimum Property Requirements (MPRs)

These standards help ensure the property is safe, sound, and livable.

6. Loan Underwriting

During underwriting, the lender reviews the borrower’s:

- income

- credit history

- debt-to-income ratio

- documentation supporting the loan application

This step ensures the loan meets VA and lender guidelines before final approval.

7. Closing on the Home

Once the loan is approved, the transaction moves to closing.

At closing:

- final documents are signed

- funds are transferred

- ownership of the home is recorded

Important Buyer Protection: The VA Escape Clause

VA purchase contracts typically include a VA escape clause, which protects the buyer if the home’s appraised value comes in lower than the purchase price.

If the appraisal is lower than expected, the buyer may be able to cancel the contract without penalty, depending on the situation and contract terms.

This safeguard helps ensure veterans do not overpay for a property based on inflated pricing.

VA Offer Strength Playbook: How to Win Against Conventional Buyers

many Veterans worry that using a VA loan will make their offer less competitive than conventional financing. In reality, most of the hesitation from sellers comes from misunderstandings about how VA loans work.

Common Seller Myths About VA Loans

Some sellers believe VA offers mean:

- The loan will take longer to close

- The appraisal will kill the deal

- Buyers can’t afford closing costs

- The process is more complicated

In most cases, these concerns come from outdated information. With proper preparation, VA buyers can present strong, competitive offers.

How to Strengthen a VA Offer

A well-prepared offer can help reduce seller concerns and increase the chances of acceptance.

1. Get a strong pre-approval

A detailed lender pre-approval shows the seller that your financing has already been reviewed. Some lenders also offer pre-underwritten approvals, which can strengthen credibility.

2. Offer a competitive earnest money deposit (EMD)

Earnest money demonstrates serious intent to purchase.

Home Price | Typical EMD Range |

|---|---|

| $300,000 | $3,000 - $9,000 |

| $400,000 | $4,000 - $12,000 |

| $500,000 | $5,000 - $15,000 |

A larger deposit can reassure sellers that the buyer is committed.

3. Keep documentation clean and ready

Providing organized documentation early-such as income verification and employment records-can help lenders move quickly through underwriting.

4. Flexible closing timelines

Being flexible with closing dates may make your offer more attractive to sellers who need extra time to move.

Smart VA Concession Strategy

VA loans allow certain seller concessions within program guidelines, which can reduce buyer costs.

In some transactions, sellers may agree to help cover:

- Closing costs

- Discount points to lower interest rates

- Prepaid property taxes or insurance

Strategic concessions can help buyers preserve cash while still submitting competitive offers.

With preparation and a strong lender partnership, many VA buyers successfully compete with-and often win against-conventional offers.

Compare Your VA Buying Power

Understanding how VA loan benefits affect your buying power can help you make more informed homebuying decisions.

A quick review of your eligibility and potential payment scenarios may help clarify:

- Estimated home price range

- Potential monthly mortgage payments

- Available VA loan options

- Possible closing costs and funding fee considerations

Potential Additional Buyer Credits

In certain transactions, eligible buyers who use a reAlpha real estate company may qualify to receive up to 1% credit at closing.

When combined with reAlpha Mortgage, that credit may increase to up to 1.5%, subject to eligibility and lender approval.

These credits may help offset certain closing costs depending on the specific transaction.

Explore Your Options

If you’re considering using your VA loan benefit, you can take the next step by exploring your potential buying power.

Options to get started:

- Check VA loan eligibility

Explore homes

Reviewing these options can help you better understand how VA financing may support your homeownership goals.

Get the latest market trends, homebuying tips, and insider updates—straight to your inbox. No fluff, just the good stuff.

Article by

Rocky Billore is a mortgage industry leader and Chief Sales Officer with over two decades of experience across residential and commercial lending. Since entering the industry in 2004, he has been directly involved in funding more than $1.4 billion in loans. A recognized expert in VA and government lending, Rocky combines deep program knowledge with a data driven, relationship-first leadership style. His work focuses on building scalable sales organizations, developing high performing teams, and aligning technology with real world lending outcomes to improve the homeownership experience.